Top 50 Threats Today

Know the worst threats and where they're lurking in your systems, with this free guide.

Key takeaways

Financial crime risk management (FCRM) is the practice of proactively looking for financial crime, including investigating and analyzing suspicious activity, rooting out vulnerabilities and taking steps to lower an organization’s risk of becoming a victim.

For organizations in every industry across the globe, an effective FCRM strategy has never been more important. Almost all organizations are doing business online, increasing attack surfaces and making businesses easy targets for cyber threats and cybercrime. Criminals are adopting more stealthy and sophisticated approaches to access critical financial data and cover their tracks.

According to Kroll's 2023 Global Economic Crime and Fraud Survey, 60% of surveyed executives predict an increase in global financial crime over the next 12 months, putting the onus on organizations to protect their data from both external and internal threats and ensure that they’re compliant with regulatory laws. If organizations fail to take the necessary steps to identify and combat financial crime, they could face stiff penalties that reach into the millions and even billions of dollars.

In this article, we’ll look at:

We’ll also look at ways you can establish protective measures to mitigate your risk of being a victim of financial crime.

In simplest terms, financial crime is the practice of taking money or property illegally from another person or organization for one’s benefit.

Among the major types of financial crime are:

These crimes can be executed both by external attackers or internal employees, including leaders at the very top of the business.

Financial crime also incorporates a range of less-serious criminal activities. While the cost or legal ramifications may not be as high as with the major types listed above, the following behavior falls under the umbrella of financial crimes:

Meanwhile, financial crime perpetrators tend to range from petty thieves to heavy-hitting global crime syndicates:

(Corporate espionage poses a substantial risk, learn how to protect yourself.)

Financial crime compliance is the process of ensuring that your organization is meeting the standards, policies and regulations (both internal and external) that apply to your industry and organization.

In 1990, the U.S. Department of the Treasury established the Financial Crimes Enforcement Network (FinCEN), which lays the groundwork for financial crime compliance:

Financial crimes have a significant impact on an organization’s revenue — but so can remaining compliant. According to a study performed by LexisNexis, the global cost of financial crime compliance topped $274 billion in 2022, up from $213.9 billion in 2020. That means the global cost has soared 28% in just a couple years.

(LexisNexis 2022 Global Summary)

As financial crimes increase, costs are expected to continue rising into 2023.

With constant changes in technology, increases in financial crimes and expanding regulations, maintaining compliance can be an ongoing battle. As an example, recent trends have made achieving anti-money laundering (AML) compliance substantially more difficult.

The United Nations estimates that the amount of money laundered in one year is 2% to 5% of global GDP or $2 trillion in current US dollars. Because of this, organizations need to meet stringent anti-money laundering (AML) compliance requirements — otherwise, they might face heavy penalties.

However, AML compliance is becoming increasingly difficult to achieve for several reasons, including:

To help achieve AML compliance, companies should:

A financial crime risk assessment is a systematic, step-by-step process of analyzing an organization’s vulnerability to financial crime. To perform a financial risk assessment, you’ll need to take the following steps:

Identify your risks: You need to both understand and document risks, based on the complexity of your organization, the market you are in, the services and products you provide, and how much of your business is conducted online. Looking at past incidents within your organization, and the general proliferation of these financial crimes in the market, you’ll need to estimate your risk level for each of the following:

Once you have documented your risks, you can prioritize them, based on which pose the biggest threat.

Establish protective measures to mitigate your risks: With full awareness of where you are most vulnerable, you can plan the controls and systems that you will implement to prevent financial crimes within and against your organization. These controls can include:

Review and improve controls: Your organization should conduct regular audits to ensure that the controls you have put into place are addressing new risks. As the market and overall environment changes, you need to create new procedures and policies to address new issues and ensure compliance.

Monitor and report: You must monitor the effectiveness of your controls, so document suspicious activity and the steps you’ve taken to resolve the issue. Proper reporting is required under various compliance regulations, so it’s critical to have that information readily available.

FCRM tools enable security staff to proactively identify potential vulnerabilities, examine activity continuously, perform ongoing risk assessments, and manage and respond to questionable activity. Here’s a breakdown of their capabilities:

FCRM systems help combat financial crime in two ways — they clear away much of the noise so analysts can focus on financial crime prevention strategy and compliance, and they offer better visibility and insight while alerting analysts when suspicious behavior occurs.

Here is how FCRM technology helps to prevent these common crimes:

The laws set the precedent for how your organization can prevent and address financial crimes within your organization. Knowing which rules apply to you, monitoring changes in the laws, and building awareness about them across the organization are your top priorities.

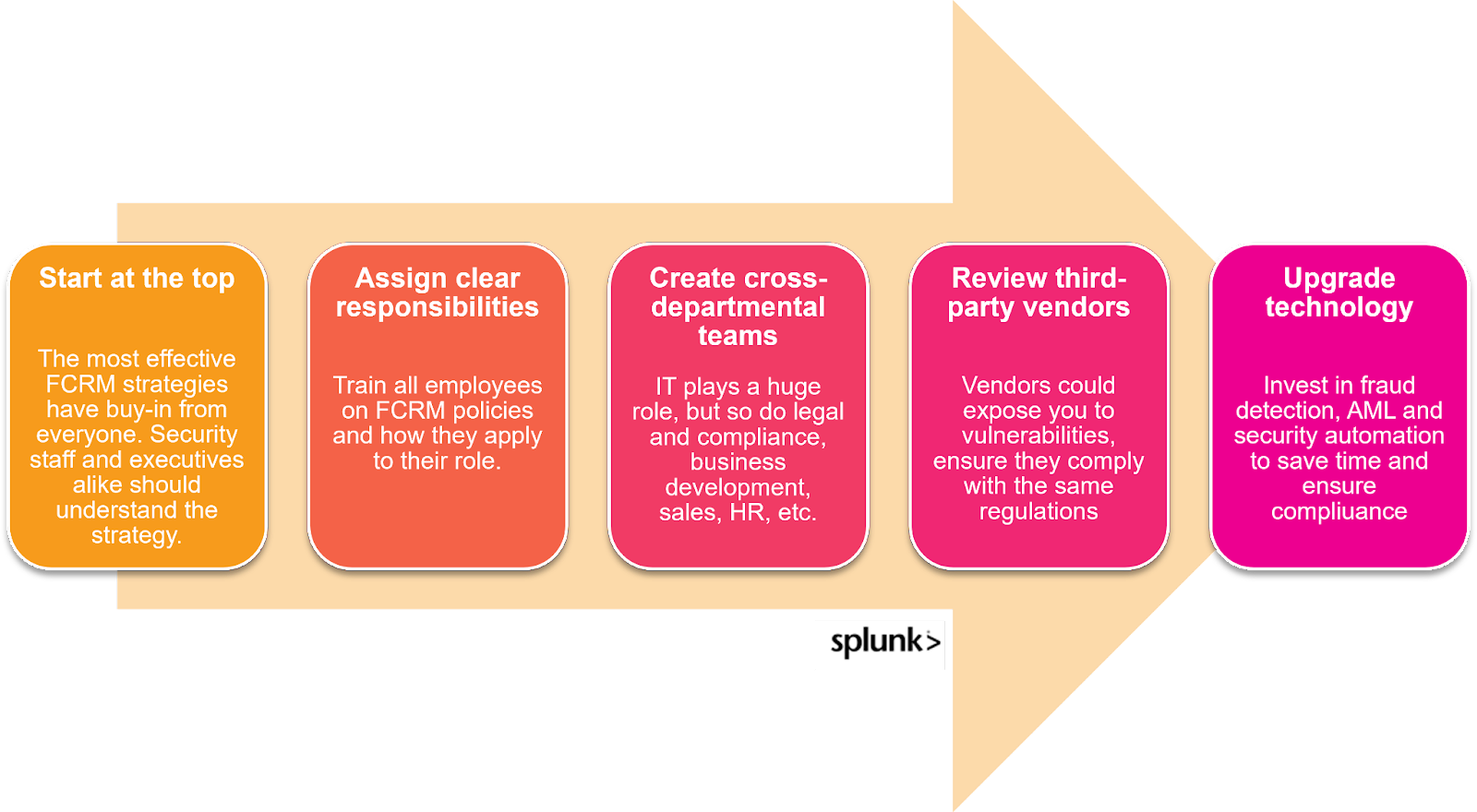

These best practices will also help you prevent criminal activity:

(We broke down how to manage risk with third-party vendors and implement security automation.)

When it comes to choosing an FCRM solution, the platform you choose will be heavily dependent on your needs, making it imperative to conduct a thorough risk assessment before you begin researching tools. Here are some of the features you’ll also want to consider:

Customers expect a safe, real-time, omni-channel experience. E-commerce and digital data transactions create new challenges in assessing and managing your financial crime risk. That said, this isn’t something you can put off or ignore.

Regulators will hold your organization responsible for any financial crimes that happen on your watch, even those that come from outside forces. Adopting an FCRM solution makes it easier to identify, respond to and prevent those threats, while ensuring that your organization remains compliant — even with a growing and increasingly complex array of regulations.

See an error or have a suggestion? Please let us know by emailing splunkblogs@cisco.com.

This posting does not necessarily represent Splunk's position, strategies or opinion.

The world’s leading organizations rely on Splunk, a Cisco company, to continuously strengthen digital resilience with our unified security and observability platform, powered by industry-leading AI.

Our customers trust Splunk’s award-winning security and observability solutions to secure and improve the reliability of their complex digital environments, at any scale.

Get the latest articles from Splunk straight to your inbox.

© 2005 - 2025 Splunk LLC All rights reserved.